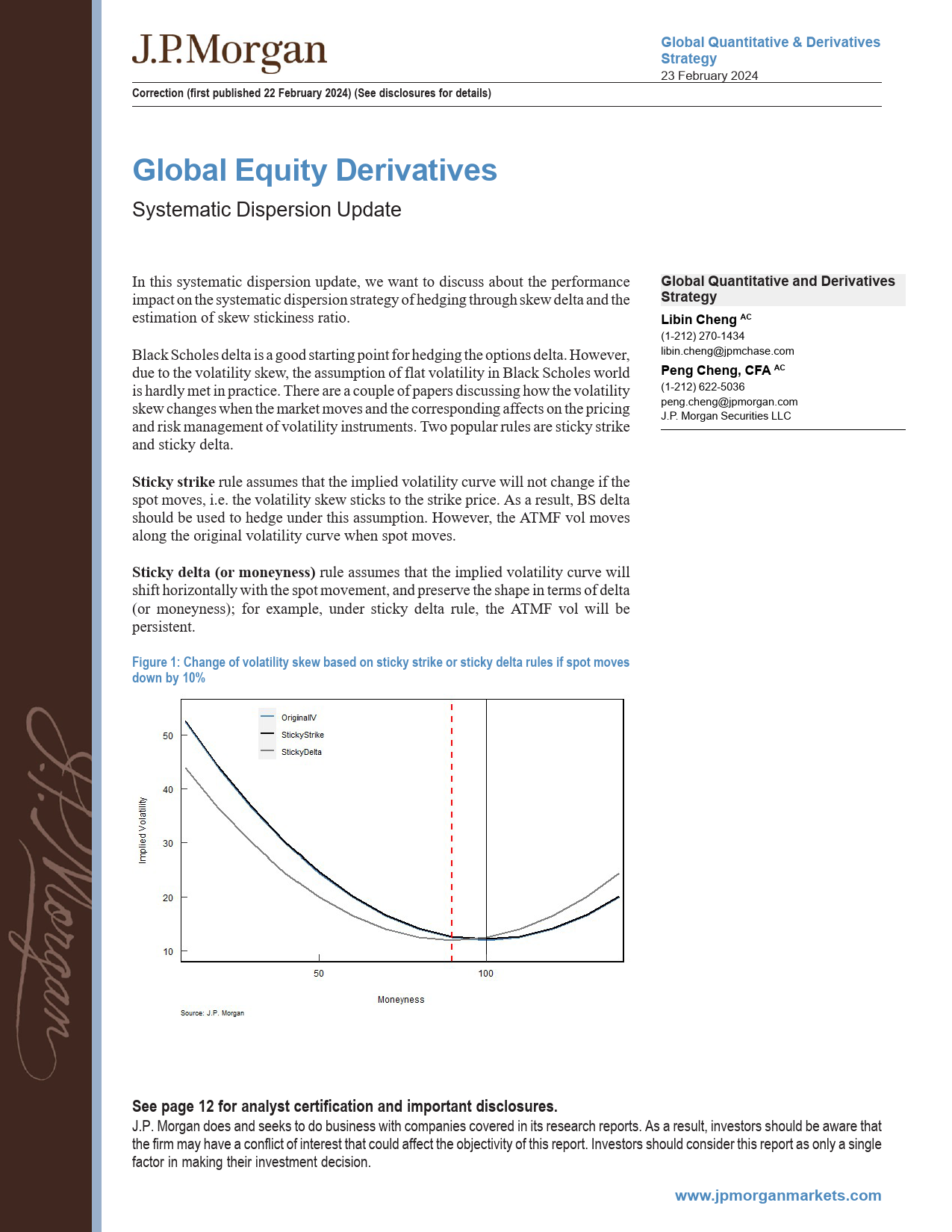

JPMORGANGlobalQuantitative&DerivativesStrategyCorrection(firstpublished22February2024)(Seedisclosuresfordetails)23February2024GlobalEquityDerivativesSystematicDispersionUpdateInthissystematicdispersionupdate,wewanttodiscussabouttheperformanceGlobalQuantitativeandDerivativesimpactonthesystematicdispersionstrategyofhedgingthroughskewdeltaandtheStrategyestimationofskewstickinessratio.LibinChengACBlackScholesdeltaisagoodstartingpointforhedgingtheoptionsdelta.However,duetothevolatilityskew,theassumptionofflatvolatilityinBlackScholesworld(1-212)270-1434ishardlymetinpractice.Thereareacoupleofpapersdiscussinghowthevolatilitylibin.cheng@jpmchase.comskewchangeswhenthemarketmovesandthecorrespondingaffectsonthepricingandriskmanagementofvolatilityinstruments.TwopopularrulesarestickystrikePengCheng,CFAACandstickydelta.(1-212)622-5036Stickystrikeruleassumesthattheimpliedvolatilitycurvewillnotchangeifthepeng.cheng@jpmorgan.comspotmoves,i.e.thevolatilityskewstickstothestrikeprice.Asaresult,BSdeltaJ.P.MorganSecuritiesLLCshouldbeusedtohedgeunderthisassumption.However,theATMFvolmovesalongtheoriginalvolatilitycurvewhenspotmoves.Stickydelta(ormoneyness)ruleassumesthattheimpliedvolatilitycurvewillshifthorizontallywiththespotmovement,andpreservetheshapeintermsofdelta(ormoneyness);forexample,understickydeltarule,theATMFvolwillbepersi...

发表评论取消回复